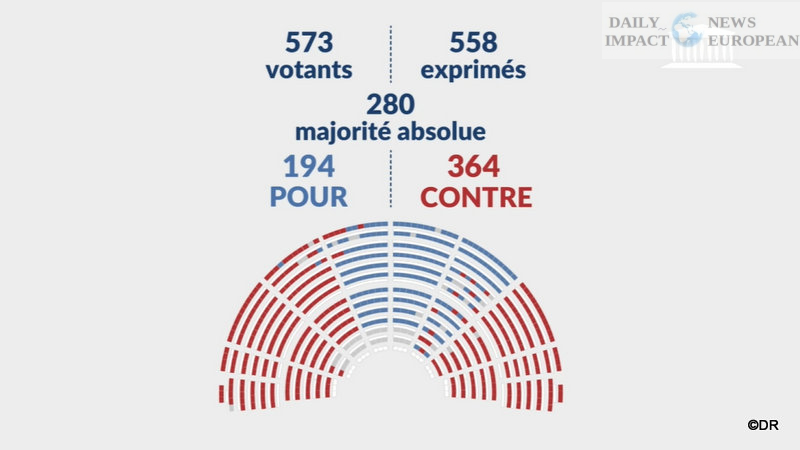

The French government has been ousted by a large majority in Parliament, following a confidence

vote tied to deficit reduction efforts.

A total of 364 lawmakers voted to dismiss the government, while only 194 supported it. According to

an Élysée Palace statement, the government will formally resign on Tuesday morning.

President Emmanuel Macron has no public address scheduled tonight, and his options remain

limited. Reluctant in recent weeks to dissolve the National Assembly, he is expected to appoint a

new Prime Minister — his fifth in just one year and eight months. Another, less likely, option would

be to call early presidential elections, something Macron has ruled out as his mandate runs until

2027.

The political crisis comes in the wake of a bill introduced by François Bayrou to reduce the budget

deficit, which stood at nearly 6% of GDP last year. The plan called for €44 billion in spending cuts

by 2026, including the elimination of two public holidays. Nevertheless, the government’s fall will not

halt the nationwide strike planned for September 10, driven by anger over Bayrou’s austerity

measures, shrinking purchasing power, and the fragile state of the French socio-economic model.

Marine Le Pen, leader of the far-right National Rally (RN), the largest party in Parliament, urged

Macron to call snap elections, recalling that he himself had made that decision last year.

Opposition leaders had already announced they would vote to oust the government, leaving

Macron with no choice but to appoint a new Prime Minister. The President, however, has reiterated

that he will neither dissolve Parliament nor call early elections, unlike last year.

Macron’s centrist alliance lost its absolute majority three years ago and has since been forced to

rely on coalitions or govern as a minority, as in Bayrou’s case. The RN now holds the largest bloc in

Parliament but remains unable to govern alone. Political instability threatens France’s ability to

bring down its deficit, raising the risk of a credit rating downgrade. Last year, the deficit stood at

nearly 6% of GDP — double the 3% target set by the EU — while public debt reached 114% of

GDP.

The government’s collapse comes at a sensitive time for Europe, which seeks to play an active role

in peace talks between Russia and Ukraine, while facing trade frictions with the United States and

mounting competition from China.

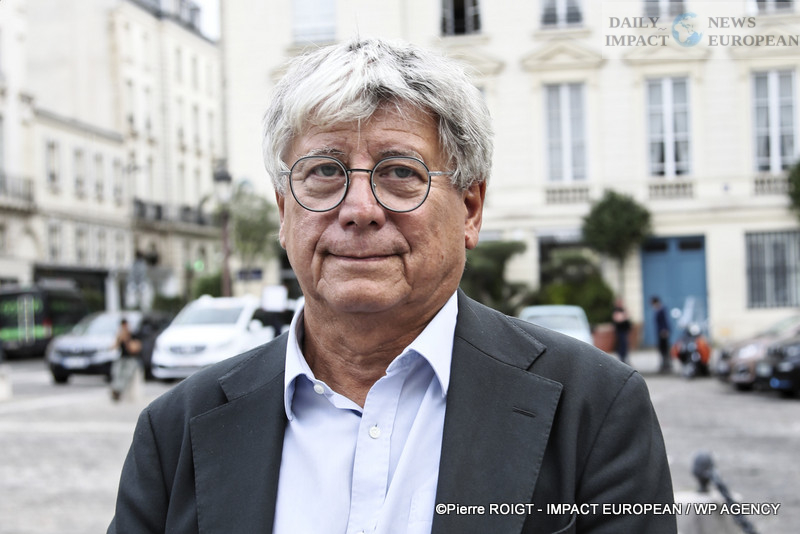

“At the European level, Brussels relies heavily on France. The real danger is not within the EU

itself, but in a potential loss of investor confidence in France. The country is financed not only by its

citizens but also by foreign funds, such as pension funds investing in French public debt. If Brussels

detects waning confidence, the contagion could spread across the eurozone, which would be

catastrophic — especially amid growing geopolitical tensions with the United States,” said

economist Jean-Luc Ginder.

According to him, France must act quickly:

“At this pace, €110 billion in net savings would be needed to restore fiscal balance. This is

achievable, provided public spending is reduced and people agree to work more in order to boost

the economy.”

Debt servicing costs, already soaring, are set to reach €100 billion a year by the end of Macron’s

term. If the trend continues, the IMF could step in and impose harsh reforms, similar to those

experienced by Greece, including a 15 to 20% cut in pensions. “That would mark the end of

national sovereignty,” Ginder warned.

“France must act — and act fast. Deficit reduction is an absolute priority. Lower growth means

higher deficits, and ultimately it is French workers who will finance the social model. This will require

deep, painful, but necessary reforms,” the economist concluded.

©2025 – IMPACT EUROPEAN

Views: 1

More Stories

Paris “Iftar of Peace”: Imam Hassen Chalghoumi awards Olive Branch Peace Prize to President Donald Trump

Global Nuclear Energy Summit in Paris highlights role of nuclear power in energy transition

Super League: Wigan Warriors defeat Toulouse Olympique 36-16